India Paper Production Market Report Regional Capacity Analysis & Market Dynamics 2018-20 vs 2024-25

MARKET ANALYSIS

10/4/20256 min read

Executive Summary

The Indian paper manufacturing landscape has undergone a dramatic transformation between 2018-20 and 2024-25, characterized by significant regional consolidation and capacity rationalization. Total national production capacity witnessed marginal growth, masking substantial geographic shifts in manufacturing hubs.

Key Finding: Maharashtra and Gujarat have emerged as dominant production centers, collectively accounting for approximately 58% of national capacity by 2024-25, while traditional manufacturing states like Tamil Nadu and Punjab experienced significant capacity contractions.

This report provides comprehensive analysis of state-wise production trends, identifies growth drivers and decline factors, and offers strategic insights for industry stakeholders navigating this evolving market landscape.

1. Market Overview

India's paper industry has experienced a period of strategic reconfiguration from 2018-20 to 2024-25. While aggregate national capacity growth has been modest, the geographic distribution of production capacity has shifted dramatically, reflecting evolving competitive advantages across states.

The industry has witnessed concentration of capacity in western India, particularly Maharashtra and Gujarat, driven by superior infrastructure, policy support, raw material availability, and proximity to key consumption centers. Concurrently, traditional manufacturing hubs in southern and northern India have experienced capacity rationalization.

1.1 National Production Capacity Trends

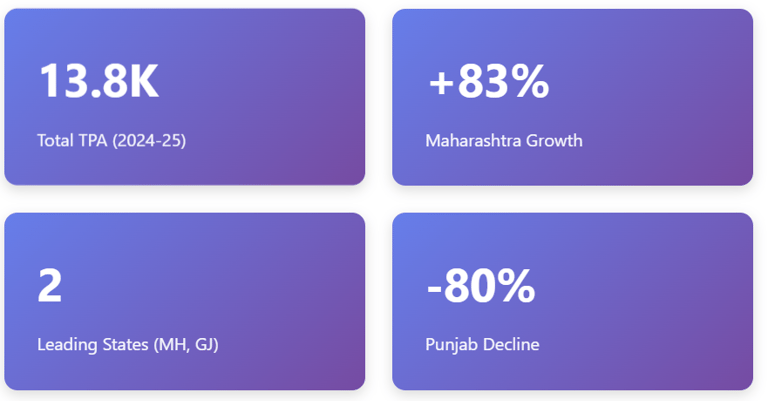

Estimated total production capacity stood at approximately 13,800 thousand TPA in 2024-25, compared to roughly 13,900 thousand TPA in 2018-20, representing a marginal 0.7% decline. However, this aggregate figure conceals significant inter-state variations.

2. State-wise Production Analysis

3. Growth Leaders: Strategic Analysis

3.1 Maharashtra: The Manufacturing Powerhouse

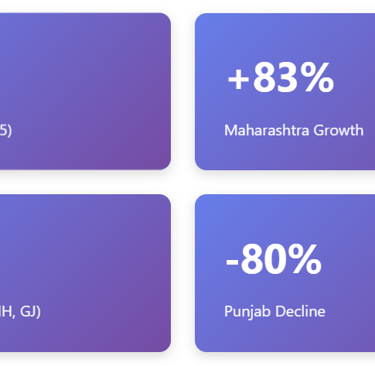

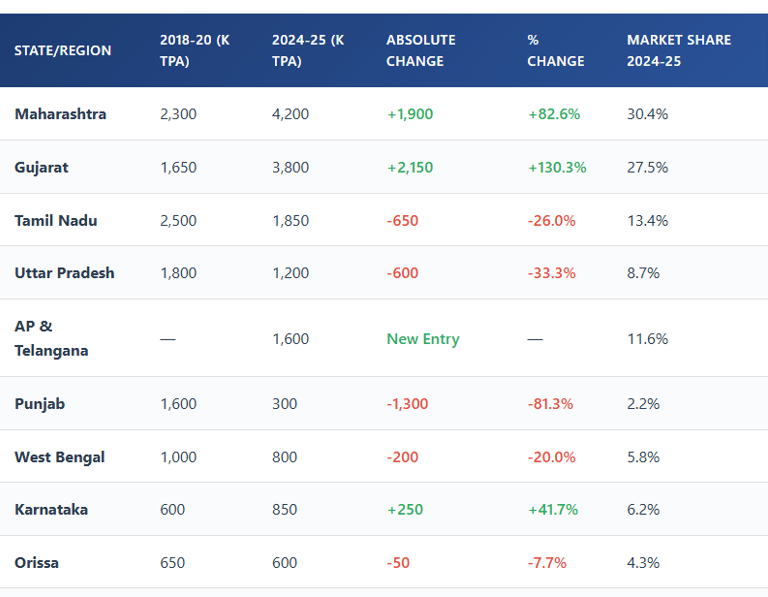

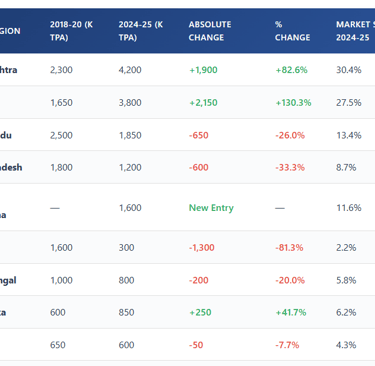

Maharashtra has solidified its position as India's premier paper manufacturing hub, with capacity surging by 83% from 2,300k TPA to 4,200k TPA. This remarkable expansion reflects several competitive advantages:

Strategic Location: Proximity to major consumption centers including Mumbai metropolitan region and access to western and northern markets

Infrastructure Excellence: Well-developed port facilities (JNPT, Mumbai Port), road networks, and rail connectivity facilitating raw material imports and finished goods distribution

Policy Support: Progressive industrial policies, streamlined approvals, and investment-friendly regulatory environment

Raw Material Access: Established supply chains for both domestic waste paper and imported pulp

Industrial Ecosystem: Presence of allied industries, skilled labor pool, and established manufacturing clusters

Strategic Insight

Maharashtra's growth trajectory suggests continued capacity additions are likely through 2027-28, particularly in packaging paper and board segments driven by e-commerce growth and FMCG sector expansion. Infrastructure investments in Nagpur-Pune industrial corridor will further enhance competitive positioning.

3.2 Gujarat: The Rising Star

Gujarat's 130% capacity expansion (1,650k to 3,800k TPA) represents the most dramatic growth story in the Indian paper sector. The state has transformed into a manufacturing powerhouse through:

Aggressive Industrial Policy: Single-window clearances, subsidized land allocation, and tax incentives attracting major investments

Port Infrastructure: Kandla, Mundra, and Hazira ports providing cost-effective access to imported recovered paper and pulp

Power and Water: Reliable industrial power supply and water resource management supporting 24/7 operations

Manufacturing Clusters: Development of dedicated paper manufacturing zones with shared infrastructure

Export Orientation: Strategic positioning for Middle East and African export markets

3.3 Andhra Pradesh & Telangana: The New Entrant

The emergence of AP & Telangana as a distinct production center with 1,600k TPA capacity (likely redistributed from historical AP data) indicates strategic importance of southern manufacturing belts. Key factors include:

Coastal Access: Visakhapatnam and Krishnapatnam ports facilitating raw material imports

Renewable Energy: Abundant solar and wind power reducing operational costs

Labor Availability: Skilled workforce at competitive wage rates

Southern Market Access: Proximity to Karnataka, Tamil Nadu, and Kerala consumption centers

3.4 Karnataka: Steady Growth

Karnataka's 42% capacity increase (600k to 850k TPA) reflects moderate but sustained expansion. Bangalore's position as a major consumption center and the state's IT/ITES sector growth driving packaging paper demand support this trajectory.

4. Capacity Decline States: Causal Analysis

4.1 Punjab: The Dramatic Contraction

Punjab's 81% capacity collapse (1,600k to 300k TPA) represents the most severe decline in the sector. Multiple structural factors contributed:

Water Crisis: Depleting groundwater tables and stringent water allocation policies making paper manufacturing economically unviable

Environmental Regulations: Increased pollution control requirements and effluent treatment costs

Power Costs: Higher industrial power tariffs compared to western states eroding competitiveness

Raw Material Logistics: Landlocked location increasing transportation costs for imported pulp and waste paper

Competition: Inability to compete with scale advantages of Maharashtra and Gujarat mills

Mill Closures: Several small and medium-scale units permanently shuttered operations

Industry Implication

Punjab's decline signals that environmental sustainability, particularly water availability, will increasingly determine long-term viability of paper manufacturing locations. States with water stress may experience further capacity rationalization unless closed-loop water systems and alternative fiber sources are adopted.

4.2 Tamil Nadu: The Southern Shift

Tamil Nadu's 26% capacity reduction (2,500k to 1,850k TPA) is significant given its historical prominence. Contributing factors include:

Power Costs: Higher electricity tariffs compared to western states impacting operational economics

Water Scarcity: Recurring droughts and competing water demands from agriculture sector

Regulatory Pressure: Stringent environmental norms and NGT directives affecting mill operations

Competition: Loss of competitive advantage to newer, larger-scale facilities in other states

Technology Gap: Aging machinery in some mills versus modern facilities in Gujarat and Maharashtra

Despite decline, Tamil Nadu retains significant capacity (1,850k TPA) and remains an important regional player, particularly in writing and printing paper segments serving educational institutions and publishing industries.

4.3 Uttar Pradesh: Northern Rationalization

UP's 33% capacity decline (1,800k to 1,200k TPA) reflects closure of smaller, inefficient units unable to compete with larger integrated mills. However, the state retains strategic importance given its large population and consumption potential.

4.4 West Bengal and Orissa: Moderate Declines

West Bengal (20% decline) and Orissa (8% decline) have experienced modest capacity reductions primarily affecting smaller mills. Both states retain potential for revival given raw material availability (bagasse, bamboo) and port access (Kolkata, Haldia, Paradip).

5. Strategic Implications & Market Outlook

5.1 Structural Shifts

The data reveals profound structural transformation in India's paper industry:

Regional Consolidation: Manufacturing capacity concentrating in states with superior infrastructure, policy support, and resource availability

Scale Advantages: Larger, integrated mills gaining market share at the expense of smaller units

Coastal Advantage: States with port access enjoying cost advantages in raw material procurement

Environmental Imperatives: Water availability and environmental compliance emerging as critical determinants of long-term viability

Technology Modernization: Newer mills in Gujarat and Maharashtra incorporating advanced technology providing productivity and quality advantages

5.2 Demand-Supply Dynamics

Despite modest national capacity growth, India remains a paper-deficit nation, importing approximately 2-3 million tons annually. Key demand drivers include:

Packaging Paper: E-commerce boom, FMCG growth, and retail expansion driving corrugated box and packaging board demand

Writing & Printing: Education sector and government consumption providing stable base demand

Specialty Papers: Growing demand for industrial and specialty grades

Tissue Products: Rising consumption of hygiene products in urban markets

5.3 Investment Opportunities

High-Potential Areas

1. Maharashtra & Gujarat Expansion: Both states offer conducive environment for greenfield and brownfield capacity additions, particularly in packaging grades

2. Specialty Paper Manufacturing: Untapped potential in high-value specialty grades currently imported

3. Backward Integration: Pulp manufacturing and waste paper recovery infrastructure investments

4. Technology Upgrades: Modernization of existing facilities in Tamil Nadu and northern states to restore competitiveness

5. Sustainable Practices: Water recycling, renewable energy integration, and alternative fiber development

5.4 Risk Factors

Raw Material Volatility: Dependence on imported waste paper and pulp creating price volatility and supply chain risks

Environmental Regulations: Stricter norms potentially increasing compliance costs and limiting expansion in certain regions

Water Availability: Growing water stress threatening operations in several states

Digital Disruption: Continued decline in newsprint and cultural paper demand due to digitalization

Import Competition: Cheap imports from Southeast Asia and China pressuring domestic prices

6. Market Outlook 2025-2030

6.1 Capacity Addition Forecast

Based on announced projects and market dynamics, we anticipate:

National Capacity Growth: 3-4% CAGR through 2030, reaching approximately 16,000-17,000k TPA

Maharashtra: Additional 1,000-1,200k TPA by 2030, primarily in packaging grades

Gujarat: 800-1,000k TPA capacity additions focused on export-oriented production

Southern States: Selective expansions in Karnataka and AP-Telangana totaling 400-500k TPA

Technology Focus: New capacity emphasizing water efficiency, renewable energy, and waste paper utilization

6.2 Segment-wise Growth Projections

High Growth (6-8% CAGR): Packaging paper and board, tissue products, specialty papers

Moderate Growth (2-3% CAGR): Writing and printing papers

Declining (-1% to 0% CAGR): Newsprint

6.3 Policy and Regulatory Evolution

Expected policy developments influencing the sector:

PLI Schemes: Potential Production Linked Incentive schemes for paper manufacturing to boost domestic capacity

Environmental Norms: Stricter effluent discharge and air emission standards requiring technology upgrades

Raw Material Security: Policies promoting domestic pulp capacity and plantation development

Circular Economy: Incentives for waste paper collection and recycling infrastructure

Trade Policy: Calibrated import duties balancing domestic industry protection and downstream user interests

Methodology & Data Sources

Data Collection: Production capacity data compiled from industry sources, company disclosures, trade associations, and government statistics.

Time Periods: 2018-20 represents average capacity during fiscal years 2018-19 and 2019-20. 2024-25 represents estimated installed capacity as of fiscal year 2024-25.

Geographic Classification: State-wise classification based on mill locations. AP & Telangana combined due to data reporting changes post-state bifurcation.

Capacity Definition: Installed production capacity in thousand tonnes per annum (k TPA), not actual production.

Limitations: Data represents best available estimates. Actual capacity may vary due to temporary shutdowns, partial operations, or unreported small-scale units.

7. Conclusion

The Indian paper industry is undergoing a fundamental geographic and structural reconfiguration. The dramatic rise of Maharashtra and Gujarat as dominant manufacturing hubs, concurrent with the decline of traditional centers like Punjab and Tamil Nadu, reflects the sector's evolution toward scale, efficiency, and strategic location advantages.

For industry stakeholders, these trends present both challenges and opportunities. Manufacturers must carefully evaluate location decisions considering infrastructure access, resource availability, regulatory environment, and market proximity. Investors should focus on well-positioned players in growth states with modern facilities and sustainable practices.

The next five years will likely witness continued capacity concentration in western India, selective expansions in southern states with coastal access, and potential revival in states that address structural disadvantages through policy reforms and technology adoption.

Environmental sustainability, particularly water management and carbon footprint reduction, will increasingly determine competitive positioning. Mills investing in circular economy practices, renewable energy, and advanced wastewater treatment will gain sustainable competitive advantages.

Key Takeaway

India's paper industry growth story is no longer just about national capacity addition—it's about strategic positioning in the right geographies with the right capabilities to serve evolving market demands sustainably and competitively.